Over the past 2 years, we’ve helped 100+ churches launch a successful financial class. Naturally, one of the questions I get most often is: “We’re looking at Financial Peace University and True Financial Freedom. What’s the difference? Which one should we use?” And every time someone asks, I give them a relatively similar answer. But […]

About Bob Lotich, CEPF®

Having the “Money Conversation” as a Church…

Fairhaven Church wanted to help their people with money. But they’d seen how these things usually go: People leave feeling like all the church wants is their wallet. The ones already struggling feel worse. And everyone braces for impact when they hear a passage about money from stage. And that’s because money is SO personal. […]

The Easy Way to Run a Financial Class

Top Lessons from 100+ Churches Since we launched our 6-week financial class, True Financial Freedom, we’ve talked to a lot of churches about how to run an easy, well-attended financial class. And here’s what we’ve noticed: the ones that overthink it tend to stall out. The ones that actually get it done? They pick a […]

Before You Launch a Church Financial Class

5 Traps That Keep Churches From Getting Started We’ve walked a lot of churches through the process of picking and starting a financial class. Many had everything you’d think they’d need: a pastor who was on board, a volunteer ready to lead it, and even a budget set aside. Sounds good on paper—but what if […]

7 Ways Churches Are Using Their TFF Subscription

Beyond the big class: getting full value from your investment Most churches picture one thing when they think about running True Financial Freedom: a big group in a room, watching videos together for six weeks. That’s a great option. But it’s not the only one. Here’s how churches are actually using their subscription to reach […]

Who’s Paying for This?

5 Approaches to Funding a Church Class That Actually Work Here’s a pattern we’ve seen over and over: Everyone agrees their church should do something about financial discipleship. There’s initial excitement, maybe some research into options. And then it stalls on one question—“OK, but where’s the money coming from?” Depending on how your church handles […]

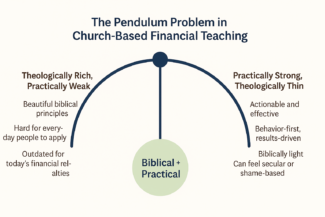

Is Your Church’s Financial Class Doing More Harm Than Good?

The hidden cost of compromise in financial discipleship—and what church leaders can do about it Churches across America have been running financial classes for decades. Yet here’s an uncomfortable question worth asking: If these classes are working, why isn’t the church becoming measurably more financially free—or more generous? The data tells a sobering story. Consumer […]

The 3 Money Dimensions

I used to think I was terrible with money. Every budget failed. Every financial plan crashed. I felt like I was constantly fighting against myself. Then I realized something: Most Christians struggle with money, not because they lack discipline. They struggle because they’re trying to be someone they’re not. Researchers (Dr. Eileen Gallo)* have discovered […]